Author

There are over 18 million US military veterans, making up about six percent of the country’s adult population.[1] Military service may make a veteran eligible for a range of retirement benefits, including a lifetime pension, disability payments, and health care, provided either through the U.S. Department of Veterans Affairs (more commonly known as “VA”) or through TRICARE, a healthcare plan administered by the Department of War (DoW).

The exact benefits a veteran receives depends on several factors including service history, tenure, disability status, and dependent status. Although the governing formulas are straightforward on paper, determining a veteran’s benefits is complex in practice and requires knowledge of both the statutory framework and the economic reasoning underlying its design. For attorneys working on personal injury cases where the plaintiff is a veteran, identifying the benefits the veteran has earned is essential to determine the reasonable value of past and future medical expenses, loss of earning capacity, and available support in wrongful death cases.

The Basic Pay Table and Retirement Annuities

The cornerstone to calculate both the pay and allowances of active duty servicemembers and the annuity for retirees is the basic pay table, which sets monthly pay according to a servicemember’s grade and years of military service. In 2002, the 9th Quadrennial Review of Military Compensation determined that military pay should be set at or above the 70th percentile of their civilian peers, where “peers” are defined by age and educational attainment. The basic pay table changes annually according to the Employment Cost Index, a dataset maintained by the U.S. Bureau of Labor Statistics that tracks the hourly labor costs of employers.[2] Congress can make changes to the basic pay table beyond these annual raises as it did in early 2025[3], but such changes do not retroactively change a veteran’s pension annuity, which is solely determined by the basic pay received during his or her tenure in the armed forces.

Under current DoW rules, there are two primary retirement systems available to servicemembers depending on when they entered service. Either retirement system requires 20 years of service for active-duty (or “Regular”) members to qualify for benefits. The requirements for non-Regular members (i.e., Reserves/Guard) are more complex and depend not only on tenure, but whether each year of service meets certain criteria.[4] There is no prorated pension benefit for those with less than 20 years of active duty or the equivalent Reserve/Guard credits.

Servicemembers who began their military careers before January 1, 2018, are covered by the legacy retirement system: a defined-benefit pension equal to 2.5 percent of their “retired pay base” – typically the average of their highest 36 months of basic pay for each year of service. Thus, a servicemember retiring after 20 years would receive a monthly payment of 50 percent of their retired pay base, a person retiring after a 30-year career would receive 75 percent, and so on with a maximum of 100% of their basic pay at 40 years of service.

Those entering service on or after January 1, 2018, participate in the Blended Retirement System (BRS). Though similar in structure, the BRS pension multiplier is slightly lower at 2.0 percent per year of service, resulting in a smaller guaranteed pension at 20 years of service. However, BRS includes a defined-contribution component through the Thrift Savings Plan (TSP), with the DoW matching contributions that become vested over time. Thus, the retirement income for post-2018 servicemembers depends not only on their grade and tenure, but also on how much the member saved under the TSP and how financial markets perform.[5]

To illustrate, take two Army Soldiers: say the first is a Lieutenant Colonel (LTC) in the Army (i.e., O-5 pay grade) retiring with 20 years of service and, second, a Master Sergeant (MSG) (i.e., an E-8 grade), retiring with 25 years of service. Under the legacy retirement system, their retirement annuity would be calculated as follows:

- The LTC would receive 50 percent of his or her basic pay; an O-5 with 20 years of service currently receives $11,592.30 in monthly pay.[6] Thus, the LTC’s retirement annuity would pay $5,796.15 per month in retirement.

- The MSG would qualify for a higher percentage of the active duty pay (i.e., 62.5 percent). An E-8 with over 24 years of service, receives monthly pay, $7,207.80. Thus, the MSG’s retirement annuity would pay $4,504.88 per month in retirement.

The BRS will complicate these calculations, as retirement annuities will also depend on servicemembers’ contributions and market performance.

Disability Compensation

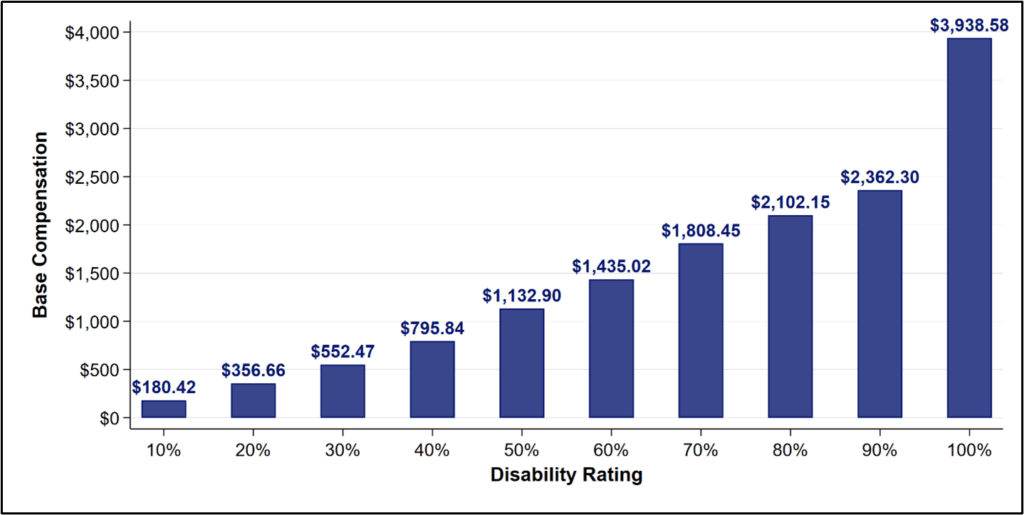

Although retirement pay is only available to servicemembers that have served for at least 20 years, there are no such tenure requirements on disability pay. After separating from the military, those whose service caused or aggravated a disability receive a monthly stiped from the VA where the exact amount depends on their disability rating. Ratings range from 0% (no disability) to 100% (full disability), and, if their rating is greater than 30%, the payment also takes into account their dependent status. The US Census estimates that there were 5.4 million veterans receiving a total of $112 billion in disability pay as of 2022.[7] The figure below shows the base compensation by disability rating for servicemembers without dependents in 2026.

Source: https://www.veteransunited.com/network/military-disability-compensation-rate-tables/

These payments can increase if the disabled servicemember’s household includes dependents, like a child, spouse, or parents. A complete table of the disability payment schedule can be found on the va.gov website.[8] Regardless of the exact amount, it is important to note that these payments are not taxed and, thus, any damage calculations should take into account their tax advantage as well.

Veterans’ Healthcare Benefits: The VA and TRICARE

Upon retirement, veterans may be eligible to receive health services through the VA health system. Eligibility for VA health care is determined by many factors but depends primarily on discharge status and whether the veteran has a service-connected disability. Higher disability ratings typically confer stronger access to care and lower out-of-pocket costs.[9] In contrast to private insurance, VA health benefits are delivered directly through VA medical centers and clinics, with the government acting as both payor and provider.

Separately, many current service members, military retirees, and their eligible family members receive healthcare benefits through TRICARE, the DoD’s health insurance program. TRICARE pays for care provided by military treatment facilities and by the civilian facilities and practitioners that commercially insured patients use. TRICARE has several plans, including TRICARE Prime, a managed care option in which all active-duty members must enroll, and TRICARE Select, a self-managed preferred provider organization (PPO). Which plan a servicemember, dependent, or retiree uses is determined by geography, age, and personal choice. For example, TRICARE Prime Demo is only available in designated Prime Service Areas. TRICARE for Life, a Medicare wrap-around coverage, is only available to those eligible for Medicare. Unlike active-duty personnel, retirees are not required to enroll in TRICARE Prime.

In a litigation context, determining whether a veteran’s medical care is provided by the VA, covered under TRICARE, or paid by another insurer is critical. Health care costs depend on which program is responsible for payment. Assuming VA or TRICARE benefits pay for all services in all cases can result in incorrect estimates of allowed amounts. Attorneys handling medical billing disputes or personal injury cases involving veterans must carefully distinguish between VA-provided care, TRICARE coverage, and any supplemental private insurance to make sure veterans’ health benefits are properly accounted for in each matter.

Key Documents for Military and Veteran Benefits

Attorneys assessing a plaintiff’s eligibility for military retirement, VA benefits, or TRICARE coverage should request the following documents. Each record serves a distinct purpose in determining service history, disability status, and health-care eligibility. The plaintiff’s written authorization is required to obtain any of these documents.

To establish military service and retirement eligibility:

- DD 214/DD 215 – the DD 214 is the foundational record of active-duty service, showing dates of service, character of discharge, pay grade, and wartime service. DD 215 reflects official corrections. The document(s) can be obtained through the National Archives (eVetRecs) or through the veteran’s VA.gov records portal at: https://vetrecs.archives.gov/s/.

- Retirement Points Statement – this document is a chronological record of creditable service points used to determine eligibility for retired Reserve and National Guard members. These records must be obtained from the proper Service, not through the VA or DoW portals.

- 20-Year Letter – the 20-year letter formally confirms that a Reserve or Guard member has completed 20 qualifying years toward non-Regular retirement. The letter is issued by the member’s Reserve or Guard component, and copies are maintained in their personnel file.

- Retiree Account Statement – this is a monthly Defense Finance and Accounting Services (DFAS) statement that confirms the retiree is receiving his or her annuity, showing the payment amount and type of retirement. The statements can be downloaded from the DFAS website, at https://mypay.dfas.mil/#/.

To establish VA disability, health care eligibility, or VA pension eligibility:

- VA Rating Decision Letter – the official document showing whether the veteran has a service-connected disability and the assigned percentage rating. It can be recovered from the VA.gov disability claims portal.

- VA Benefits Verification Letter (“Summary of Benefits”) – the verification letter is a simplified, downloadable document showing current disability rating and benefits received. It is also available through the VA.gov web portal.

- VA Health Care Enrollment Documents – these records confirm enrollment in the VA health system and the veteran’s assigned priority group. It can also be downloaded though the VA.gov web portal.

To establish TRICARE eligibility and enrollment:

- DEERS Enrollment Record – the DoW’s database record indicating whether the veteran and dependents are eligible for TRICARE. Relevant documentation can be downloaded by the veteran from https://milconnect.dmdc.osd.mil/milconnect/.

- TRICARE Enrollment – also available through milConnect, active and retired servicemembers can obtain proof of their and their dependents’ TRICARE health coverage.

Conclusion

Taken together, these benefits form a complex patchwork of income streams, health insurance coverage, and eligibility rules that can be difficult to navigate without specialized knowledge of military compensation systems. Whether the issue at hand involves valuing a veteran’s long-term financial security, determining the allowed amount for a medical bill and which entity is responsible for paying a medical bill, or accurately calculating loss of income, even small misunderstandings about these benefits can lead to substantial errors.

RPC’s economists have deep experience analyzing military pay and benefits, including their legal and economic implications, and can provide expert analysis or testimony to ensure the finder of fact correctly understands the veteran’s compensation and health benefits in litigation contexts. Before joining RPC in 2025, Economist and Senior Consultant, Sam Absher, PhD, worked as an economist at RAND Corporation, studying – among other topics – military compensation, recruiting, and retention. In that role, he provided research supporting the 14th QRMC[10], which recommended changes to the 70th percentile benchmark in the 9th QRMC. The 2025 National Defense Authorization Act (NDAA) ultimately provided across-the-board pay raises to servicemembers with targeted raises to junior enlisted servicemembers.[11]

[1] Katherine Schaeffer, “The changing face of America’s veteran population,” Pew Research Center, November 8, 2023.

[2] https://www.bls.gov/eci/

[3] https://veteran.com/2025-military-pay-charts/

[4] A complete description of the requirements for non-Regular servicemembers is outside the scope of this blog, but a detailed description can be found in DoD 7000.14-R: https://comptroller.war.gov/Portals/45/documents/fmr/current/07b/07b_01.pdf

[5] https://militarypay.defense.gov/pay/retirement/

[6] https://www.dfas.mil/MilitaryMembers/payentitlements/Pay-Tables/Basic-Pay/CO/

[7] https://www2.census.gov/library/publications/2024/demo/acs-58.pdf

[8] https://www.va.gov/disability/compensation-rates/veteran-rates/

[9] For a full explanation of VA eligibility criteria, see: https://www.va.gov/health-care/eligibility/

[10] The RAND Report which Dr. Absher co-authored can be found on RAND’s website at the following link: https://www.rand.org/pubs/research_reports/RRA2400-1.html

[11] https://armedservices.house.gov/news/documentsingle.aspx?DocumentID=4889

To learn more, contact Sam Absher, PhD. To discuss a case, contact Athenna Dill, CPC, Personal Injury Case Manager at 512.371.8005 or adill@rpcconsulting.com.

Learn More About RPC’s Loss of Earning Capacity Services and Medical Billing Analysis